How to Structure Retirement Income Planning for Modern Life Expectancy

Could there be a downside to medical advances, healthier lifestyles, and better healthcare access?

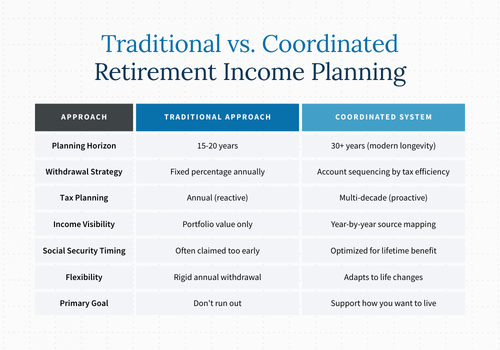

In their massive contribution to today’s longer lifespans, these three factors have led to retirements that routinely span 30 years or more. Yet, most retirement planning still uses assumptions from previous generations, with shorter timelines, outdated tax structures, and an understanding of lifespans that no longer reflect reality.

As a result, retirees who saved diligently now face uncomfortable questions in their 70s and 80s:

- Will our savings last?

- Is this healthcare expense affordable?

- What can we actually afford to leave behind to our loved ones?

- Should we have planned differently?

A 30-year retirement isn't just a longer version of what worked before. It requires a different financial structure entirely.

The risks compound differently. The tax exposure doesn’t accumulate in the same way. The strategies that were safe for a shorter retirement—withdraw 4%, adjust when needed, hope the portfolio holds—aren't designed to withstand three decades of market volatility, inflation, rising healthcare costs, and tax drag.

Modern life expectancy has fundamentally changed retirement income planning.

What Happens When A Retirement Plan Isn't Coordinated For Today's Realities?

Take a couple entering retirement with $3 million in retirement savings.

They've done everything right: maxed out their retirement accounts, lived below their means, avoided debt, and saved well.

Their advisor tells them they can retire earlier than most and withdraw $100,000 a year to cover living expenses. The math works. The projections look fine. They feel ready.

In the first few years of their retirement, everything feels manageable. They claim Social Security. Withdrawals cover expenses. They pull from their IRA when they need cash, and from their taxable account when the market's up.

It all feels smooth.

What they don't see—what most people don't see—is the erosion happening beneath the surface.

By claiming Social Security at 62, they've locked in a permanently reduced benefit amount that will compound over 30 years. What seemed like a practical decision has permanently lowered their guaranteed income for the rest of their lives.

And those IRA withdrawals that felt manageable? They're pushing the couple into higher tax brackets and triggering provisional income thresholds that make 85% of their Social Security benefit taxable.

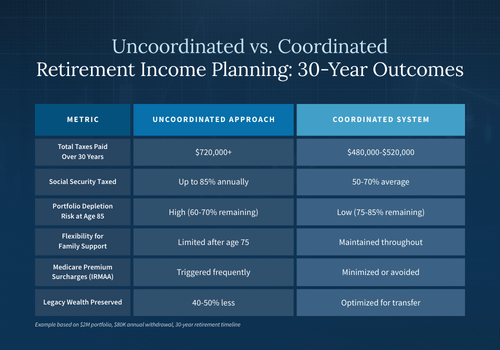

Without a withdrawal strategy to coordinate across account types, they're depleting the wrong accounts at the wrong time, paying more in taxes than necessary every year, and leaving themselves increasingly exposed to sequence-of-return risk as their portfolio shrinks and spending needs remain unchanged.

None of these decisions feel catastrophic in isolation. But over 30 years, they compound.

The couple that seemed financially secure enough to retire early starts feeling pressure at 78. By 85, they're making hard choices about long term care, travel, and whether they can help their grandchildren with college.

The money that should have lasted comfortably is running thin because their retirement income strategy wasn’t built to coordinate financial planning with the reality of a longer life.

The Better Way to Plan Retirement Income

There's a better approach.

Retirement income planning can be built as a coordinated system from the start—one that accounts for modern longevity, tax implications, and the reality that sufficient income needs to work for 30+ years, not 15.

This framework replaces generic withdrawal rates with year-by-year income mapping that shows exactly where every dollar comes from. It pulls from the right accounts in the right order to minimize tax implications and reduce portfolio vulnerability when sequence-of-return risk is highest. And it treats taxes as a multi-decade reality.

The decisions you make in your 60s protect your spending power in your 80s.

Retirement income planning stops being a withdrawal-rate formula and becomes a structure designed to support how you actually want to live—for as long as you live.

This is the framework that turns longevity from a risk into a reality you're prepared for.

How Seaside Wealth Management Delivers This System

This coordinated approach to retirement income planning is what Seaside Wealth Management develops and delivers.

A Spending Plan Built for Modern Longevity

Our process begins with understanding what matters: your lifestyle expectations, your health and longevity assumptions, your plans for travel or family support, and your tolerance for uncertainty.

Those priorities shape everything we build together.

Whether you want to retire early, need long term care coverage, or plan to maintain your current lifestyle while supporting loved ones, we start with your specific retirement goals.

Year-by-Year Income Strategy Mapping

From there, we map your income sources year by year across the full retirement timeline.

Every source—Social Security, portfolio withdrawals, pensions, cash reserves—is coordinated into a clear, year-by-year plan that shows exactly where your income comes from and how it adapts as circumstances change.

This isn't a static projection. It's a dynamic investment strategy that accounts for inflation, market volatility, and life changes, updated as your situation evolves.

We address how to manage investments across different accounts, when to claim Social Security to maximize your benefit, and how to create sufficient income to cover both essential living expenses and discretionary expenses throughout retirement.

A Withdrawal Strategy Designed to Make Money Last

That means withdrawal sequencing is built into that framework from the start.

We identify which accounts to draw from in which years to minimize tax implications, preserve portfolio longevity, and reduce early-retirement vulnerability.

If it makes sense to delay Social Security until full retirement age and live off taxable accounts in your 60s, the retirement plan reflects that. If Roth conversions during lower-income years can reduce your tax burden over the next two decades, that's mapped out with specific timing and amounts.

A Tax Strategy That Protects Your Cash Flow

This is all part of a tax strategy that’s integrated into every decision.

We account for how withdrawals affect Social Security taxation, how RMDs will impact Medicare premiums and Medicare Advantage coverage, and how provisional income thresholds compound across decades. The framework also addresses estate tax implications to protect what you pass to loved ones.

The goal is to structure income in a way that protects your spending power from the tax drag that most retirees never see coming.

This is the system Seaside Wealth Management delivers: a coordinated income framework built for 30+ year retirements, designed to evolve as your life evolves, and structured to make your money last as long as you do.

What Changes When Retirement Income Is Planned To Last

A coordinated retirement income system creates both financial and psychological transformation.

Financial Clarity Creates Flexibility

The strategic withdrawal sequencing we outlined above preserves assets for later stages of retirement.

Drawing from taxable accounts first reduces future RMDs and creates tax-free income options when long term care costs rise or healthcare coverage needs change. Your portfolio doesn’t just last longer, it's positioned to support different needs at different stages.

A Coordinated Plan Supports Life, Not Just Withdrawals

With a framework that accounts for specific goals, retirees are able to help children with a home purchase, fund a grandchild's education, or support aging parents without undermining long-term security.

This extends beyond family responsibility. For instance, some clients maintain part time work in early retirement, which the plan integrates to take advantage of continued income and delayed Social Security claiming.

Anxiety Turns To Confidence

We know the fear of running out of money won’t disappear just because someone says "you'll be fine."

It disappears when you can see the structure, follow a specific plan, and see how coordination is built to last. With Seaside Wealth’s retirement framework, you stop worrying about whether your money lasts and start focusing on living well, knowing your finances are structured to support the rest of your life.

The New Standard for Retirement Income Planning

Traditional retirement income planning was built for shorter retirements and simpler tax structures. It worked when most Americans had pensions and retirements lasted 15 years.

It doesn't work for 30-year retirements.

Modern longevity requires a coordinated system that integrates Social Security timing, withdrawal strategy, and tax planning into a unified framework designed to last as long as you do. Seaside Wealth Management builds that structure as a long-term partnership that evolves with your life.

The consequences of entering retirement without a coordinated income framework won’t reveal themselves immediately. But the decisions made today—about withdrawals, Social Security timing, tax strategy—can silently compound against you for three decades.

Don't wait until your late 70s to discover your income plan wasn't built to last.

Schedule a conversation with Seaside Wealth Management today and build a retirement income plan for your specific goals and the timeline modern longevity demands.

Read More

5 Retirement Investment Strategies for Modern Longevity

How the Right Retirement Planning Services Determine Whether Your Savings Last

Why $1 of Extra Income Can Cost You $5,000 In Retirement Tax Planning

How Outdated Estate Planning Can Cost The Family It Was Meant To Protect

How Social Security Timing Can Make A $600K Difference in Taxes