The Truth About Tax-Free Retirement

A tax-free retirement.

It sounds great, doesn't it?

After decades watching a portion of every paycheck go to the IRS, the idea of never paying taxes again feels like the ultimate win.

But even retirees who move 100% of their assets into tax-free retirement accounts face tax exposure from multiple sources:

- Social Security benefits become taxable based on provisional income formulas.

- Medicare premiums spike when income crosses IRMAA thresholds.

- State tax codes treat retirement income differently depending on source and timing.

And that’s when the problem compounds.

Cross the wrong income line and taxes don’t just take a slice, they inflate Medicare premiums, phase out healthcare subsidies, and quietly turn every withdrawal into a more expensive decision than it looks on paper.

That’s why it’s important to clarify…

Yes, you can pay zero federal income tax on your retirement income.

But that outcome isn’t achieved with a single retirement tax strategy or planning around a single year of retirement.

It requires a tax-minimization framework that integrates every income source, account type, and tax threshold into one system that ensures you pay the lowest possible taxes over your lifetime.

It might not sound quite as catchy as “tax-free retirement,” but by coordinating Roth conversions with withdrawal sequencing, employing provisional income management, and planning for multi-decade tax brackets, you can preserve more of your wealth across multiple decades.

What Happens When Retirees Don’t Have A Coordinated Plan?

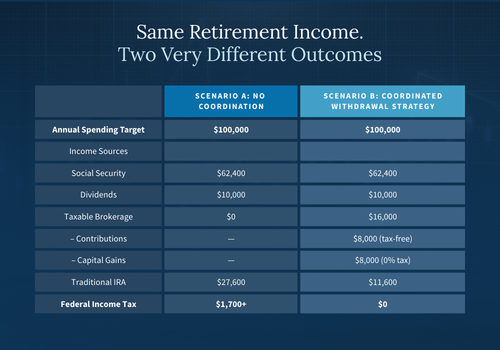

Consider a couple in their late 60s living on $100,000 annually.

They have $62,400 in Social Security, generate $10,000 in dividends, and need another $27,600 to meet their spending goals.

Most retirement DIYers would pull the full $27,600 from their traditional IRA.

But every dollar from the IRA is taxed as ordinary income, which increases provisional income and makes more of their Social Security taxable.

That would mean a $1,700+ tax bill.

How To Minimize Taxes Across Your Lifetime

The issue isn’t that this couple can’t afford their retirement.

They have enough savings to live off $100,000 a year and live the lives they want.

The issue is that they’re treating retirement income as a single-year problem instead of a 30-year system. They haven’t planned when to pull money, which accounts to use first, or how much taxable income they can safely generate each year without triggering cascading taxes.

Once you reframe retirement that way, the solution becomes connected to a bigger plan.

Rather than withdrawing $27,600 entirely from their traditional IRA, the couple in the scenario described above reduce their tax hit by drawing $16,000 from a taxable brokerage account—$8,000 in original contributions and $8,000 in capital gains—and covering the remaining $11,600 from the IRA.

This leads to $0 federal income tax.

The capital gains are taxed at 0% for their income level, and the lower IRA distribution keeps Social Security taxation minimal.

Same lifestyle. Same $100,000 income.

But with a $1,700 difference in annual taxes just from knowing which accounts to use.

How Seaside Wealth Management Builds Tax-Minimization Frameworks

These tax savings don’t come from chasing a single tactic or planning one year at a time.

They come from a coordinated, comprehensive retirement plan.

At Seaside Wealth Management, we build a complete system for your retirement that maps every income source—Social Security, investment income, retirement accounts—and then coordinates how they interact across decades.

This multi-account system reduces total lifetime taxes with strategies that can lead to zero federal income taxes on retirement income.

That system includes:

Timing Roth Conversions to Low-Income Windows

Between retirement and Social Security benefits, many retirees have lower income (no pension yet, Social Security unclaimed, modest portfolio withdrawals). That's when Roth conversions cost least. Once required minimum distributions begin, income increases structurally and conversion opportunities shrink.

Seaside Wealth Management maps these windows in advance, identifying exactly when conversions make sense based on projected income from all sources.

Sizing Conversions to Avoid Bracket Spikes and Penalties

Conversions create taxable income. Too large, and they push into higher tax brackets or trigger IRMAA surcharges.

We size conversions to stay below thresholds, spreading them across multiple years. A large conversion executed as several smaller conversions often produces significantly lower total taxes than a single-year conversion.

Using Bridge Accounts to Extend Conversion Windows

For clients retiring before Social Security claiming age, we establish "bridge accounts."

These taxable accounts are strategically structured to fund early retirement years while creating maximum space for Roth conversions.

By withdrawing from taxable accounts first, clients preserve tax-deferred balances for conversion during low-income years.

Capital gains from these withdrawals are often taxed at 0% and don't inflate provisional income the way traditional IRA distributions do.

This sequencing extends the conversion window by 5-10 years for many retirees, allowing larger total conversions at lower lifetime tax costs.

Integrating With Total Income Strategy

Conversions are one variable in a system that includes Social Security timing, withdrawal sequencing, and provisional income management.

If a client delays Social Security, that extends the conversion window.

If a client needs early income, we’ll sequence withdrawals from taxable accounts first, preserving tax-deferred accounts for conversions.

If a one-time income event occurs—business sale, inheritance, property sale—we’ll model the impact on Medicare premiums and Social Security taxation, then adjust the conversion schedule accordingly.

This level of coordination can produce years with zero federal income tax liability by strategically balancing withdrawals and minimizing traditional IRA distributions to stay below taxation thresholds.

But those zero-tax years only work because they're part of a multi-decade plan that manages total lifetime taxes.

What Changes With Lifetime Tax Planning

The advantage of this approach shows up in two enormous ways.

Flexibility to Respond to Life Changes

Multi-account coordination lets retirees adapt to one-time events, tax law changes, and unexpected expenses without triggering penalties.

More Wealth Preserved for What Matters

Minimizing taxes across decades keeps more assets invested longer, extending portfolio longevity, avoiding IRMAA surcharges, and reducing Social Security taxation.

The outcome isn’t always zero taxes.

But it will result in lower taxes across 30 years, more control over timing, and fewer surprises from thresholds and surcharges that most retirees don't discover until the bill arrives.

Get A Tax Strategy Built for How Retirement Actually Works

"Tax-free retirement" makes for a great headline.

But the reality of retirement tax management requires understanding how Social Security, Medicare, and withdrawals collide year after year.

Seaside Wealth Management provides retirement tax strategies grounded in that reality.

We build a system that creates more tax-free income in retirement and preserves more of a retiree’s savings for the rest of their life.

That complete system coordinates Roth conversions with withdrawal sequencing, Social Security timing, and multi-decade income planning to reduce total lifetime taxes.

If that’s what you want for your retirement, here’s what we recommend:

1. Schedule a consultation with Seaside Wealth Management.

2. Review your tax strategy with us and see how coordination across account types and decades can reduce your lifetime tax burden.

3. Get stronger control, better wealth preservation, and more flexibility for the rest of your life.

Read More

Why $1 of Extra Income Can Cost You $5,000 In Retirement Tax Planning

How Social Security Timing Can Make A $600K Difference in Taxes

7 Gift Tax Strategies for Helping Adult Children Without Ruining Your Retirement

5 Roth IRA Conversion Strategies To Prevent Six Figures In Taxes

26 Things To Consider In 2026