5 Roth IRA Conversion Strategies To Prevent Six Figures In Taxes

Too many retirees are walking into the same tax trap.

They retire in their 60s and their tax bracket drops to 10% or 12%. Financial advisors mention Roth conversions, but there's no urgency, so nothing gets done.

And then, at 73, required minimum distributions begin.

Suddenly the IRS is forcing $60,000+ out of their traditional IRA annually, taxed as ordinary income, which pushes their tax bracket to 22%. Social Security becomes 85% taxable. Medicare premiums double.

By 83, they're paying six figures in taxes for a decade on money they didn't even need to withdraw.

And the worst part is, there's no turning back. The window to prevent this closes at 73.

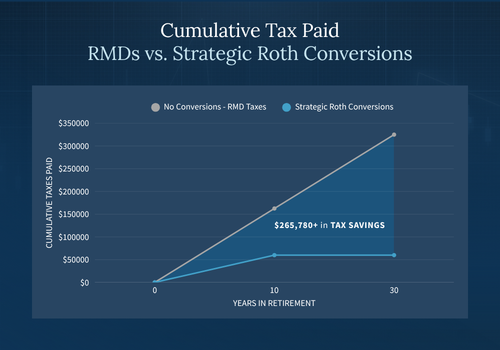

What you do in the years before could determine whether you pay $60,000 or $325,000 in taxes over the next 30 years.

That's why this article is as timely as it is important. Strategic Roth IRA conversions during the gap years between retirement and 73 allow you to convert traditional IRA dollars at 12% instead of paying 22-37% on forced distributions for decades.

Below, we identify five strategies that help you capture those savings and avoid losing your retirement to poor timing and unintended penalties.

1. Fill The 12% Bracket Before RMDs Force You Into Higher Brackets

The first and most powerful Roth IRA conversion strategy targets the window we mention above—between retirement and 73—when tax brackets are widest and income is lowest.

The Risk

During early retirement, most affluent retirees find themselves in the 10% or 12% marginal tax bracket for the first time in decades.

With no wages and Social Security delayed or just starting, living on cash reserves or taxable account withdrawals generates minimal taxable income. That means the 12% bracket has tens of thousands of dollars in unused capacity.

But at 73, that capacity disappears. RMDs begin, calculated as a percentage of your traditional IRA balance.

A couple with $1.5 million in pre-tax retirement accounts faces RMDs starting around $60,000 annually, rising each year. Those distributions are taxed as ordinary income, pushing retirees from the 12% bracket into 22% or 24%, where they stay for the rest of their lives.

This tax bill isn't temporary. It's permanent.

The higher ordinary income increases how much Social Security gets taxed, triggers IRMAA surcharges on Medicare premiums, and pushes capital gains from 0% into 15%.

The effective cost of that first RMD cascades across every other income source.

How To Prevent It

The strategy is straightforward: fill the 12% bracket every year before RMDs eliminate the space entirely.

Run a current-year tax projection. Identify your marginal tax bracket. Calculate the gap between your current taxable income and the top of the 12% bracket ($100,800 for married couples filing jointly in 2026).

If your taxable income this year is $40,000, you have $60,800 of space in the 12% bracket. Convert exactly that amount from your traditional IRA to your Roth account. The Roth conversion is taxable in the year you execute it, but you pay 12% on dollars that would otherwise be taxed at 22-24% as RMDs later.

Repeat this process annually.

Over 10 years, you'll have moved hundreds of thousands—potentially the entire balance—from traditional to Roth at the lowest rates you'll see in retirement.

2. Convert During Market Downturns To Maximize Shares Moved At Lower Tax Cost

The first strategy determines when to convert. The second determines the best time within that window to execute.

Many retirees convert based on tax bracket capacity or annual planning cycles, ignoring market conditions and missing an opportunity to capture more value from every conversion dollar.

The Opportunity

Roth IRA conversions are taxed on the dollar amount you convert, which means the number of shares that dollar amount represents changes with market conditions.

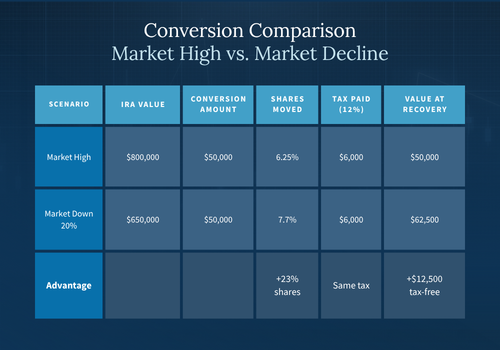

A $50,000 conversion when your IRA is worth $800,000 moves 6.25% of your account into the Roth. That same $50,000 conversion when your IRA has dropped to $650,000 during a market downturn moves 7.7% of your account—23% more shares for identical tax cost.

When the market recovers, that full 7.7% grows tax-free in the Roth IRA.

You've converted shares that were worth $62,500 at the previous high, paid taxes on only $50,000, and captured $12,500 in additional value that will never be taxed again.

The retiree who converts $50,000 regardless of market conditions pays the same tax but captures vastly different value depending on when the conversion executes.

How To Take Advantage

If markets drop 15-20% and you're already planning Roth conversions that year, accelerate them. Convert earlier in the downturn rather than waiting for recovery. The tax bill is calculated on today's depressed value, but the shares recover inside the Roth where all future growth is tax-free.

Pair conversions with rebalancing to fund the tax payment efficiently. When you're in the 12% bracket, selling appreciated positions in your taxable account lets you realize those gains at 0% long-term capital gains rates, and those proceeds can pay the income tax on the Roth IRA conversion.

3. Delay Social Security To Extend Your Roth Conversion Window

The first two strategies control how much you convert and when you convert it. The third strategy determines how many years you have to execute those conversions.

The Risk

Social Security income counts toward provisional income, the calculation that determines how much of your Social Security gets taxed. It also increases your modified adjusted gross income, which affects IRMAA surcharges and determines what tax bracket you land in.

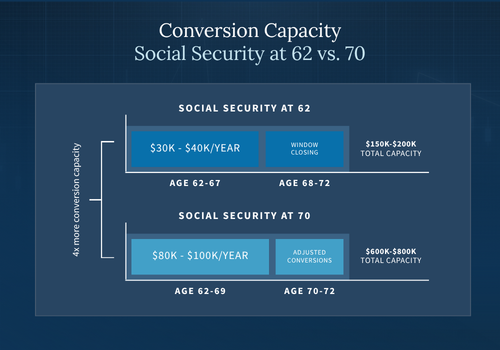

Starting Social Security at 62 adds $30,000-$40,000 annually to your taxable income immediately.

That income reduces how much you can convert to a Roth while staying in the 12% bracket, triggers provisional income thresholds that make 50-85% of your Social Security taxable, and shortens your conversion window to just 3-5 years before RMDs begin at 73.

How To Prevent It

The couple who starts Social Security at 62 might convert $150,000-$200,000 total before RMDs arrive. The couple who delays to 70 can convert $600,000-$800,000 in the same timeframe. That's 4x the capacity at the same 12% rate.

Most retirees start Social Security early because they view it as income they've earned and don't want to leave on the table. But that decision costs them conversion capacity they'll never recover, and the tax consequences can compound for decades.

Delaying Social Security to 70 provides you with eight full years (62-70) of ultra-low taxable income—no wages, no Social Security, no RMDs. Just dividends, interest, and strategic withdrawals from taxable accounts.

When considering this strategy, it's important to model the tradeoff before you make a decision.

Delaying Social Security will cost years of benefits, but it creates additional Roth conversion capacity and savings in conversion taxes. It also increases your lifetime Social Security benefit and prevents provisional income from making future benefits taxable.

For more affluent retirees with substantial traditional IRA balances, the math strongly favors delaying retirement.

4. Spread Conversions Across Multiple Years To Avoid IRMAA Cliffs

The first three strategies maximize conversion capacity. The fourth prevents a single conversion from triggering multi-year penalties that can erase the tax savings entirely.

The Risk

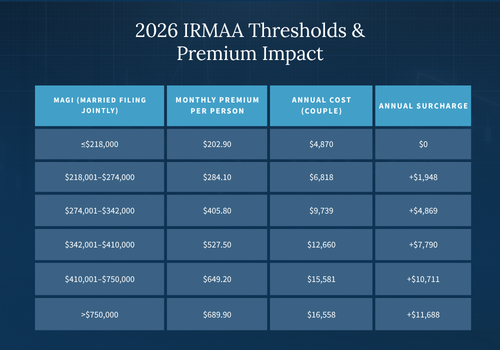

Medicare Part B and Part D premiums are income-based with standard premiums for 2026 coming in at $202.90 per month. But when modified adjusted gross income exceeds specific thresholds, IRMAA surcharges double, triple, or quintuple that amount.

For married couples filing jointly, MAGI above $218,000 triggers the first surcharge in the form of an additional $1,948 annually. Cross $342,000 and premiums jump to $7,791 per year for a couple. Part D IRMAA surcharges stack on top of these figures at every tier.

These aren't marginal increases. They're cliffs. And one dollar is enough to send you over the edge, costing thousands.

IRMAA operates on a two-year lookback, which means the penalty arrives long after the decision that caused it.

Your 2026 Medicare premiums are based on your 2024 tax return. A Roth conversion executed in 2026 that pushes MAGI above $218,000 won't show up as a surcharge until 2028.

Many retirees don't discover this until after Medicare sends the premium notice, by which point the damage is permanent and the conversion cannot be undone.

How To Prevent It

Before executing any Roth conversion, model your MAGI for the current year and the following two years. Identify where you fall relative to IRMAA thresholds.

If a planned conversion pushes you over a cliff, split it across multiple years instead.

Scenario A

A couple with $175,000 in combined income from Social Security, a pension, and portfolio distributions needs to convert $200,000 before RMDs begin in five years. They convert $100,000 in year one and $100,000 in year two, pushing MAGI to $275,000 both years.

This barely clears the second IRMAA cliff, but even one dollar over makes an enormous difference. Two years later, they pay approximately $9,738 in additional Medicare Part B premiums across those two IRMAA years — $4,869 per year — with Part D surcharges adding nearly $2,000 more.

In total, they pay approximately $11,700 across two years.

Scenario B

The same couple spreads that $200,000 conversion across all five years at $40,000 annually. MAGI stays at $215,000 each year, just under the $218,000 threshold.

No IRMAA surcharges triggered in any year.

Same total converted. A slightly longer runway. And compared to Scenario A, nearly $12,000 saved in unnecessary Medicare premiums.

Forward-looking tax modeling identifies these cliffs before you face them.

Sometimes accepting one IRMAA year makes sense if it avoids five years of higher income taxes later.

But that becomes a decision made with full visibility of the tradeoff, not a penalty discovered two years after the fact when nothing can be done to reverse it.

5. Coordinate Roth Conversions With Tax Gain Harvesting

The first four strategies determine when to convert, how much to convert, and how to avoid penalties. The fifth and final strategy maximizes the value of every conversion year by using both Roth conversions and 0% capital gains harvesting simultaneously.

The Opportunity

The 12% ordinary income tax bracket and the 0% long-term capital gains bracket operate independently, which means you can fill both in the same year without one pushing you out of the other.

A married couple can have taxable income up to $96,700 (the top of the 12% bracket) and still pay 0% on long-term capital gains, as long as total income stays under $94,050.

This creates a dual tax-elimination opportunity that many retirees miss. They look at it as an either/or scenario.

People convert traditional IRA dollars and fill the 12% bracket, leaving capital gains rates untouched. Or they harvest gains at 0% and leave conversion capacity unused.

Both approaches waste half the available bracket space.

The retiree who converts $70,000 to fill the 12% bracket has eliminated future taxes on that traditional IRA balance. But they've left $30,000-$40,000 of 0% capital gains capacity on the table.

The $150,000 in unrealized gains sitting in their taxable account will eventually be taxed at 15% when sold in higher-bracket years. That's $22,500 in future taxes that could have been eliminated.

How To Take Advantage

If your taxable income is $25,000, you have room for both a Roth conversion (taxed as ordinary income) and tax gain harvesting (0% on long-term capital gains) before hitting bracket limits.

Convert $40,000 to your Roth IRA, which gets taxed as ordinary income. Then harvest $30,000 in long-term capital gains by selling appreciated positions in your taxable account and immediately repurchasing them.

Total taxable income: $95,000 (under the 12% bracket limit).

Total capital gains: $30,000 (taxed at 0%).

You pay $8,400 in federal tax on the Roth conversion. But you've permanently eliminated taxes on $30,000 of taxable account gains by resetting the cost basis to current market value.

Future tax eliminated on those harvested gains: $4,500.

The New Standard for Roth IRA Conversion Strategy

All of the strategies presented in this article have two things in common:

1. They're about long-term thinking, making decisions that benefit the life of a retirement.

2. They will all help you avoid unnecessary taxes in isolation, but the greatest impact is when they come together as part of a coordinated plan customized to your savings.

Strategic Roth conversions require modeling across decades, not single tax years. That means identifying IRMAA cliffs two years before you cross them, coordinating conversions with market conditions and Social Security timing, and filling every dollar of low-bracket space with both conversions and gain harvesting.

Seaside Wealth Management models conversions as full, unified systems projected against future RMDs, IRMAA thresholds, and tax brackets through age 95.

The difference in outcomes is immense. Going year-by-year versus a coordinated system like this can determine whether you pay $60,000 or $325,000 in taxes over the next 30 years.

Contact us today to create a multi-year projection that shows exactly how much to convert each year without triggering penalties.

Read More

Why $1 of Extra Income Can Cost You $5,000 In Retirement Tax Planning

How Social Security Timing Can Make A $600K Difference in Taxes

7 Gift Tax Strategies for Helping Adult Children Without Ruining Your Retirement

The Truth About Tax-Free Retirement

26 Things To Consider In 2026