How Outdated Estate Planning Can Cost The Family It Was Meant To Protect

You spent 40 years saving responsibly, building meaningful wealth, and doing all the right things to leave behind something that helps the people you love.

You've taken all the steps you were told to take: A will. Maybe a trust. Beneficiaries named on retirement accounts.

Boxes checked. Drawer closed. Estate planning, done.

But what many families discover too late is that having those documents isn't the same as having a plan. When estate planning documents don't coordinate with the financial plan, the tax strategy, and the beneficiary designations behind them, the gaps show up in places no one was watching.

Assets get tied up in probate for months or years. Beneficiaries are forced to sell what they inherited just to cover the tax bill, while inheritances meant for adult children sit exposed to creditors, divorce settlements, or bankruptcy filings the family had nothing to do with. Children and loved ones are left without clear guidance, and thousands disappear into taxes that could have been reduced or avoided entirely.

For people approaching or living in retirement, every estate planning decision is also a retirement decision.

Where assets are titled determines how they're taxed during your lifetime. Beneficiary designations on a 401(k) or IRA can quietly override an entire will. A trust written before current law might force your surviving spouse into court to defend the household income.

The estate side and the retirement side should all be part of the same plan. Treating them separately is where the damage starts.

An Incomplete Estate Plan Can Cost Your Family

Imagine a couple in their late 60s. Both retired and comfortable.

They have around three million dollars spread across a brokerage account, two IRAs, a Roth, a paid-off home, and a small life insurance policy from former employee benefits.

But their estate planning consists of wills they signed in 2009, a revocable living trust they never finished funding, and beneficiary designations they last reviewed when their oldest daughter graduated college.

On paper, they look organized. They have the documents, they have an attorney's name in a folder somewhere, and they even have a living will and an advance health care directive.

What they ultimately have is a false sense of security.

When Estate Planning Documents Stop Working

The documents don't show that the brokerage account is titled jointly with their adult son, added years ago to "make things easier" for him. This single decision eliminated the step-up in basis on half the account and erased six figures of avoidable tax in one move.

The revocable trust was never retitled to own the home or the brokerage account, so both head straight into probate court. That's going to translate into 12 - 18 months of probate process, public filings, and legal fees paid out of the estate before a single dollar reaches anyone in the family.

And that's not all.

The life insurance policy still names the husband's first spouse as the primary beneficiary. The form was never updated. Beneficiary designations override every word of a will and every clause of a trust. The insurance company doesn't read intentions. It reads forms.

None of this is visible while everyone is healthy. The bank accounts, the retirement accounts, and the estate planning documents all look fine on the surface, and the errors only surface after the moment they can no longer be corrected.

How a Well-Built Estate Plan Works

The most frustrating aspect of the scenario outlined above is that it's completely avoidable.

A coordinated estate plan replaces guesswork with a single integrated system, where every legal document, account titling decision, and beneficiary designation is built to work with retirement and tax planning.

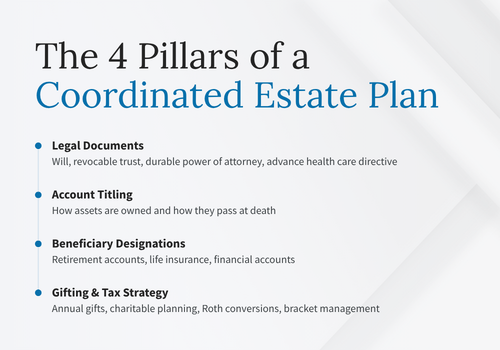

The Foundational Estate Planning Checklist

The foundation is a set of legal documents, each of which covers what the others can't.

- A last will that speaks to personal property and any assets that flow through probate.

- A revocable living trust that holds property and other assets outside the probate court entirely.

- A durable power of attorney that covers financial decisions if you become incapacitated.

- An advance health care directive covers medical decisions, including the appointment of a healthcare power of attorney to direct medical treatments and end-of-life care.

- Beneficiary designations that route retirement plans, life insurance policies, and certain bank accounts directly to the people you've named.

Those are the estate planning basics that most retirees were handed 20 years ago.

The documents are necessary, but it's nowhere near sufficient on its own.

The Financial Decision Coordination That's Almost Always Missing

The structure has to connect to the retirement plan to actually work.

- A trust that's funded with the right assets so that what should avoid probate actually does.

- Beneficiary designations that are reviewed against current intent and current law, because the rules around inherited IRAs changed substantially under SECURE Act provisions and most forms haven't caught up.

- Account titling that's evaluated for both current tax efficiency and step-up treatment at death, so a well-meaning decision to add an adult child to a brokerage account doesn't quietly erase a six-figure tax benefit.

- Gifting strategies that are coordinated with bracket management so a planned gift in one year doesn't create unintended tax liabilities in the same year, and charitable organization beneficiaries get structured to reduce estate taxes rather than treated as an afterthought.

The documents protect your wishes on paper. The coordination protects your wealth and your family from absorbing unexpected costs.

Why Current Law Matters

This is especially important because estate plans operate inside a legal process that doesn't sit still thanks to frequent updates in legislation and regulations from both state and federal governments.

The federal estate tax exemption increased to $15 million per individual in 2026 following passage of the One Big Beautiful Bill Act, up from $13.99 million in 2025. Meanwhile, state laws on probate, trust administration, and asset protection have continued to shift across the last decade as rules around digital assets, social media accounts, and access to a deceased person's financial accounts keep evolving alongside them.

A plan written before any of those changes and untouched since will still be executed when the time comes. It just won't take your intentions into account.

That means your family members could end up with tax liabilities they didn't see coming and a probate process they didn't expect to face.

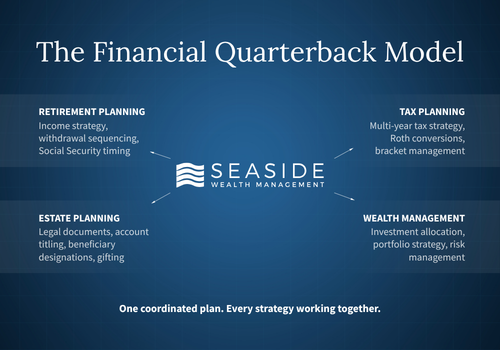

Seaside Wealth Management Keeps Your Estate and Retirement Plan Aligned

The work above isn't separate from retirement planning. It is retirement planning, done completely.

At Seaside Wealth Management, estate planning is built into the coordinated retirement framework we develop with you, not handed off to someone else and revisited once a decade.

Every estate decision you face, including funding the trust, updating beneficiary designations, evaluating gifting strategies, and coordinating with multiple beneficiaries across multiple marriages, is evaluated alongside your retirement income plan, your multi-year tax strategy, and your investment allocation.

The Financial Advisor Quarterback Model

That's an important distinction because many financial planners operate in a silo. They manage the portfolio, hand the rest to your CPA and your estate attorney, and trust that the three of you will somehow keep everything aligned across decades of life and law changes.

We work differently.

We act as the quarterback for your entire financial team, coordinating directly with your estate planning attorney and your CPA so the legal documents your attorney drafts reflect the income strategy we're executing, and the tax positions your CPA reports reflect the gifting and titling decisions your estate plan calls for.

You stop being the messenger between three professionals who each see one slice of the picture, and your professionals start working from the same plan.

That's what coordinated planning actually means in practice.

Ongoing Diagnosis, Not One-Time Review

The most expensive estate planning mistake isn't the document that was never written. It's the document that was written correctly in 2008, never revisited, and now operates under outdated tax law with beneficiary designations from a previous chapter of life.

We treat estate planning the way a family doctor treats a patient.

At every review, we run your financial vitals — beneficiaries, account titling, trust funding, gifting strategies, and the tax positions that connect them — and stress-test the plan against changes in your life, the markets, and the law.

The plan you built in your 50s still holds up in your 70s because someone is responsible for keeping it that way.

That ongoing diagnosis is what most plans never get and what most families discover they need only after it's too late to put in place.

What a Coordinated Estate Plan Actually Protects

The point of all this work is protection for the specific people you're building this for and the specific outcomes you want them to avoid.

A coordinated plan keeps a surviving spouse from liquidating retirement accounts to pay estate taxes or settle expenses tied up in probate. It keeps the inheritance you leave to adult children from being exposed to a divorcing in-law, a creditor judgment, or a bankruptcy filing they had nothing to do with. It keeps grandchildren's education funding on track by structuring 529 plans as the estate planning tool they can be, and it keeps a probate judge from appointing guardians for minor children when no parent named one in writing.

These outcomes happen routinely to families whose estate planning consisted of a will, good intentions, and a folder of important documents in a safe deposit box.

What Changes When the Plan Is Coordinated

With a coordinated plan in place, the people you're building this for receive what you intended, when you intended it, and with the structure to actually use it.

Assets pass without the probate process where the structure allows them to. Privacy is preserved because trusts don't generate public court filings. Tax liabilities are addressed during your lifetime through gifting strategies, charitable planning, and bracket-aware Roth conversions, instead of being left for your heirs to absorb after you're gone.

That's the difference between a plan that exists on paper and a plan that does what it was designed to do.

The money is the same, but the result for your loved ones is immeasurably better.

Build the Comprehensive Estate Plan Your Retirement Strategy Needs

A retirement plan that ignores estate planning isn't a complete plan. Neither is an estate plan written in isolation from the retirement strategy that supports it.

That's the work we do at Seaside Wealth Management, and it's the work behind the free, on-demand workshop Brad Lineberger and Matt Callahan recently hosted on building a lasting legacy.

Watch it now to see how wills, trusts, beneficiary designations, account titling, and tax strategy fit together into one plan to protect you, your family, and your wealth.

Read More

5 Retirement Investment Strategies for Modern Longevity

How the Right Retirement Planning Services Determine Whether Your Savings Last

Why $1 of Extra Income Can Cost You $5,000 In Retirement Tax Planning

How Social Security Timing Can Make A $600K Difference in Taxes

How to Structure Retirement Income Planning for Modern Life Expectancy