Why $1 of Extra Income Can Cost You $5,000 In Retirement Tax Planning

Most retirees spend decades carefully structuring their finances, only to fall prey to one costly, overlooked blind spot.

A poorly planned retirement tax strategy.

The problem is that in retirement, the tax code doesn't scale gradually with earnings. It sits flat, then jumps. A Roth conversion, a portfolio withdrawal, a capital gains sale you thought was routine. Nothing happens at first. But somewhere in that otherwise normal year, you crossed an invisible line, and the penalties arrive with no way to undo them.

The good news is that with a forward-looking plan, these tax thresholds become inputs to manage rather than ambushes that catch you completely off guard.

In this article, we'll walk through exactly how these tax cliffs work, why most retirees never see them coming, and the five strategies Seaside Wealth Management uses to protect your retirement income before the damage is done.

What Happens When Retirees Don't Know Where the Cliffs Are

One couple came to Seaside Wealth Management after a Roth conversion went sideways on them.

On paper, the conversion looked fine. Their income landed at $274,758, and from where they were sitting, it had been a good year.

Then the Medicare premium notice arrived, and their monthly bill jumped by $202.90 per person. More than $5,000 a year, every year the surcharge applied, because their income landed just above a threshold they didn't know existed.

They didn't make a reckless decision. They simply made an uninformed one.

What made it worse was the timing.

Medicare uses a two-year lookback to set premiums, meaning the income reported in 2026 determines what you pay in 2028. By the time the notice arrives, the tax year that caused it is long closed and nothing can be undone.

This is one tax cliff, but there are several others.

For example, up to 85% of Social Security benefits can become taxable depending on provisional income levels.

The 0% capital gains rate disappears once ordinary income crosses a specific threshold.

Additionally, the Net Investment Income Tax applies at $250,000 Modified Adjusted Gross Income (MAGI).

And for a surviving spouse, losing married filing jointly status can push the same income into a significantly higher tax bracket overnight.

Contrary to popular belief, these aren't rare tax scenarios that only affect the ultra-wealthy. For retirees drawing on tax-deferred retirement accounts, timing Roth conversions, and coordinating Social Security, they are the central terrain of retirement income taxes.

And from our experience, most retirement plans aren't built to see them coming.

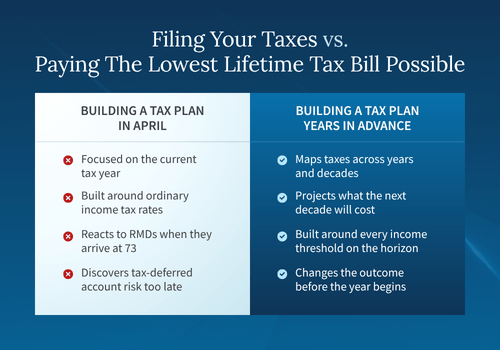

The Better Way to Approach Retirement Tax Planning

The best retirement tax plans aren't built in April around ordinary income tax rates.

They're built years in advance, with a clear picture of every income threshold and tax situation on the horizon and a strategy designed to land below each one before the year even begins.

That kind of planning requires a forward-looking model, one that traces taxes in retirement across years and decades, not just the current tax year. The tax cliffs that surface at 73 are often the result of decisions made at 65:

- When Social Security was claimed

- How much was left sitting in tax-deferred retirement accounts

- Whether Roth conversions happened gradually or all at once

A traditional IRA that felt manageable early in retirement can generate required minimum distributions (RMDs) large enough to push ordinary income into a higher tax bracket permanently, affecting Medicare premiums, Social Security taxation, and capital gains treatment all at the same time.

This isn't a problem that stems from incompetent tax professionals. Most are doing exactly what they're hired to do: reconstructing the prior year accurately and filing on time.

That work is necessary, but it's a fundamentally different job than projecting what the next decade of income decisions will cost and building a plan to change that outcome.

How Seaside Wealth Management Builds Tax Cliff Detection Into Every Plan

At Seaside Wealth Management, we build multi-year and multi-decade tax projections that model your retirement income through age 95 against every relevant threshold.

The goal is to reduce your lifetime tax drag, not just minimize this year's bill.

This approach changes what's visible, making the quiet years between retirement and Social Security a wealth-preserving window.

The RMD ramp that begins at age 73 gets mapped years in advance. IRMAA thresholds that catch most retirees off guard are built into your income targets before the year that would have crossed them.

Your Roth conversions, Social Security timing, RMD positioning, capital gains harvesting, withdrawals from tax deferred accounts, investment strategies, and charitable giving are all coordinated as one system with the sole focus of making your retirement savings last.

That means every financial decision you make for individual retirement arrangements is made with full visibility across your entire plan.

The tax cliffs that would otherwise ambush you become checkpoints in a plan that already knows they're coming.

5 Ways Seaside Wealth Management Protects More of Your Income From Tax Cliffs

Each of the following strategies targets a specific tax cliff, and while each one delivers real value on its own, the savings multiply when they're layered together as a coordinated system.

1. Spread Your Roth Conversions Across Multiple Years

A traditional IRA grows tax-deferred, meaning every dollar you eventually withdraw gets taxed as ordinary income. Many retirees try to move large amounts into a Roth IRA quickly to get ahead of future taxes. The problem is that converting too much in a single year spikes your income, pushes you above Medicare surcharge thresholds, and can make up to 85% of your Social Security benefits taxable all at once.

Spreading $200,000 in conversions across five years keeps your income below those lines each year, preserves your lower capital gains rate, and can save more than $10,000 in Medicare surcharges alone, while still moving the same amount into a tax-free Roth account.

2. Delay Your Social Security to Extend Your Conversion Window

Your Social Security claiming age doesn't have to be the same as your full retirement age.

Every year you delay claiming Social Security, your eventual benefit grows. But there's a less obvious reason to wait.

The years before your Social Security income begins are often the lowest-income years of your entire retirement, and that creates a valuable window to convert money from your traditional IRA into a Roth at a lower tax rate.

Claiming at 62 shrinks that window immediately. Delaying to 70 keeps your income low for up to eight years, creating room to convert significantly more at a 12% tax rate before Social Security income starts filling your bracket and pushing conversions into a higher one.

3. Harvest Capital Gains During Your Low-Income Years

When your income falls below a certain threshold, the federal tax rate on long-term capital gains drops to 0%. For many retirees, the gap between leaving work and the start of required minimum distributions at age 73 is the only time in their financial lives when that window is fully open.

Selling appreciated investments during these years resets their cost basis without triggering any capital gains tax. Those gains are permanently eliminated rather than deferred to a later year when your income is higher and the tax bill follows.

4. Use Qualified Charitable Distributions to Keep Your Giving Off Your Tax Return

Once you reach age 70½, the IRS allows you to transfer up to $111,000 per year (for the 2026 tax year) directly from your IRA to a qualified charity.

That gift never counts as taxable income, which means it doesn't affect your Medicare premiums, your Social Security taxation, or the surcharge thresholds that determine what you pay for Part B and Part D coverage.

For retirees who give regularly, this is one of the most effective strategies available. It also satisfies your required minimum distributions, meaning the money you were going to give away does double duty without costing you anything extra.

5. Bunch Charitable Contributions to Capture More of the Deduction

Every taxpayer can either itemize their deductions or take the standard deduction, whichever is larger.

For most retirees, spreading charitable giving evenly across years means the total never clears the standard deduction threshold, so the giving produces no additional tax benefit.

Bunching two years of giving into one year pushes total deductions above that line, capturing the full itemized benefit. In the off year, the standard deduction applies on its own. Over time, alternating between the two captures more of the deduction without changing how much you give.

The Difference a Forward-Looking Tax Plan Makes Every Single Year

Coordinating all five tax efficient strategies across a full retirement routinely produces annual savings. Over decades, the difference between a year-by-year approach and a precision-modeled retirement tax plan can reach well into six figures.

But the number that changes most people isn't the one on the projection.

It's the feeling of opening a piece of mail from Medicare and already knowing what's inside. It's April without the anxiety of wondering what this year's bill will be.

Retirement is supposed to feel like the hard part is behind you and the life you worked toward is finally yours to enjoy. When your plan already accounts for every threshold three to five years out, that's exactly how it feels.

Most Retirees Don't Know What They're Leaving Behind

Precision-level retirement tax planning isn't an optimization reserved for the ultra-wealthy. It's the baseline standard every retiree deserves, and most aren't getting it from financial advisors who spend more time looking backward than planning forward.

The decisions that determine your lifetime tax bill aren't made at tax time. They're made years earlier, and by the time they show up on a return, the window to act is already closed.

Have the income decisions you're making right now been stress-tested against the thresholds that will shape the next decade of your retirement?

That’s the question Seaside Wealth Management's analysis is designed to answer.

We project your retirement income over 30+ years and let you see exactly if and when your money will run out.

Schedule your "Will My Retirement Last?" analysis with Seaside Wealth Management today.

Read More

5 Retirement Investment Strategies for Modern Longevity

How the Right Retirement Planning Services Determine Whether Your Savings Last

How Outdated Estate Planning Can Cost The Family It Was Meant To Protect

How Social Security Timing Can Make A $600K Difference in Taxes

7 Gift Tax Strategies for Helping Adult Children Without Ruining Your Retirement