The Early Retirement Planning Guide To Cut $32K/Year In Avoidable Premiums

Retire at 67, and you step into a safety net that's already waiting for you.

Medicare covers your health insurance, Social Security replaces a portion of your monthly income, and required minimum distributions are still years away.

The system, for all its flaws, is built around retirement in your mid-60s.

Retire at 55, and none of that exists yet.

You're handling your own health coverage for a decade or more, generating income entirely from retirement savings, and making withdrawal decisions that interact with tax brackets, healthcare subsidies, and investment returns in ways that most retirement calculators never show you.

The number in your retirement accounts might look right, but without coordination across taxes, healthcare, and withdrawals, the three biggest costs in early retirement end up compounding against each other instead of being managed together.

In this article, we’re going to walk through what that coordination actually looks like, starting with a couple who retired early without it.

What Happened When Ryan and Steph Retired at 58 With $1.5 Million

Ryan and Steph retired at 58 with $1.5 million between them.

That number cleared every calculator they ran. They had no existing debt, a paid-off house, and decades of disciplined saving behind them.

By most standard measures, they were perfect candidates for early financial independence.

But being ready to retire and being ready to fund a 35-year retirement are two different things.

With no withdrawal plan and no tax strategy, they were pulling whatever covered their living expenses, whenever they needed it.

In year one, that meant $100,000 in gross withdrawals, almost entirely from pre-tax IRAs. That pushed them into the 22% bracket, subjected 85% of their Social Security retirement benefits to tax, and phased out the ACA subsidy they had been counting on for health insurance coverage.

None of this came from recklessness or poor judgment. It came from not knowing that a single pre-tax withdrawal touches your tax bracket, your healthcare subsidies, and your asset allocation all at once.

And once it does, the costs compound. Add all three together, and every dollar Ryan and Steph actually spent was costing their investment portfolio $1.42.

Five years in, the math caught up with them.

Their tax bill topped their first house's down payment. Their health care expenses were eating 20% of every withdrawal. And the savings plan that looked bulletproof at 58 was eroding faster than either of them had noticed.

That's when they came to Seaside Wealth Management.

3 Financial Mechanics That Make Early Retirement Structurally Different

What happened to Ryan and Steph wasn't bad luck. And it wasn't just a more aggressive version of the retirement risk everyone already worries about.

That $1.42 loss on every dollar traces back to three structural failures that are built into a retirement age of 58 instead of 67.

Each one is tied to a guardrail that conventional planning depends on: a paycheck, employer coverage, and a longer investment runway. Retire a decade early, and all three disappear at the same time.

1. How The Traditional IRA and 401(k) Withdrawal Trap Inflate Your Income Taxes

Every dollar pulled from a traditional IRA or an employer plan like a 401(k) counts as ordinary income the moment it lands in your bank account, taxed at ordinary income tax rates just like salary.

That income feeds a number called MAGI (modified adjusted gross income), and MAGI works like a tripwire connected to four separate alarms:

- Your tax bracket

- Social Security benefits

- Medicare premium surcharges

- ACA subsidy eligibility

Trip that wire with one large withdrawal, and all four go off at once, which is exactly what happened to Ryan and Steph the moment they pulled $100,000 out of their IRAs.

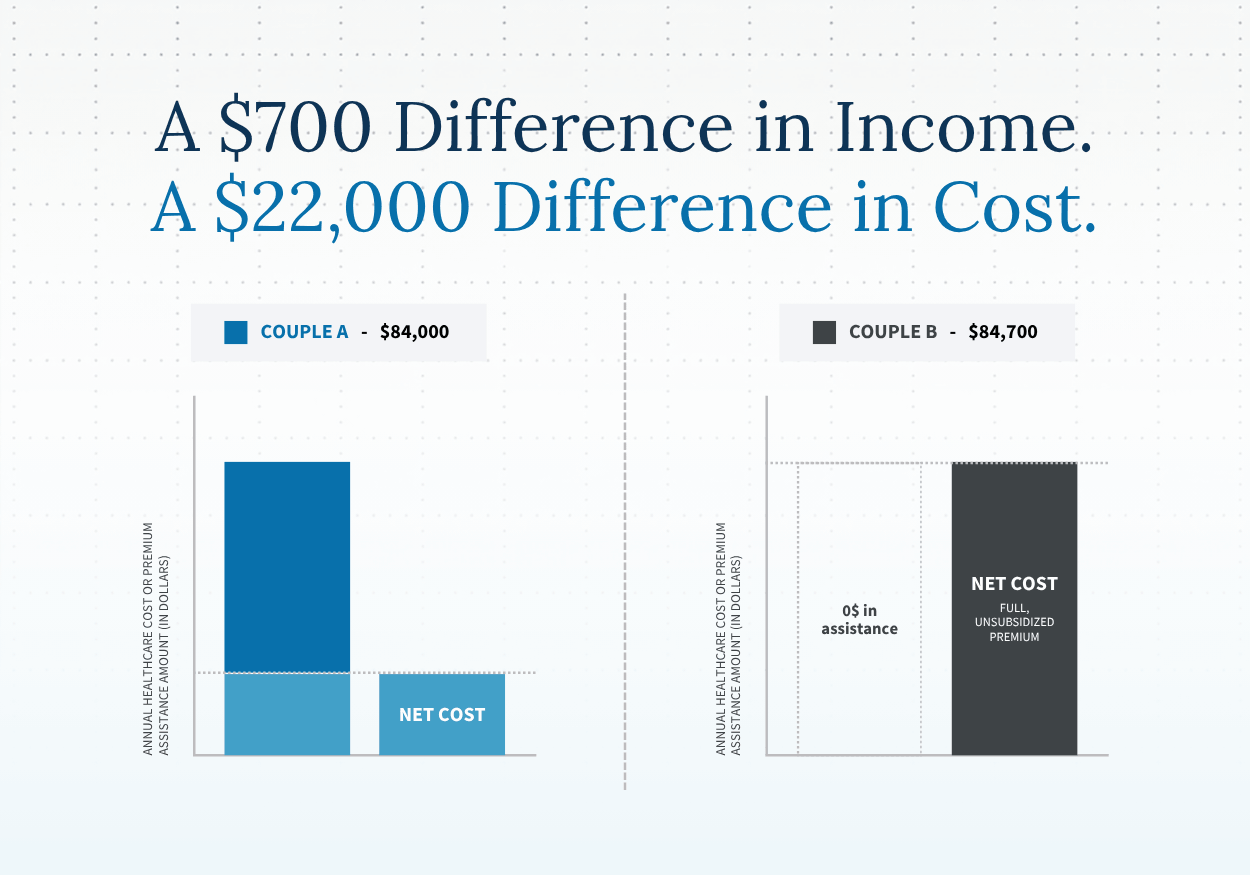

2. How the ACA Subsidy Cliff Drives Up Future Health Care Costs Before Medicare

Of those four triggers, the healthcare one is the most punishing for early retirees, because the penalty isn't gradual. It's a cliff.

ACA premium subsidies are tied to your income. Stay under the threshold and you get thousands a year in premium assistance. Cross it by even a few hundred dollars and you lose every dollar of that assistance, paying full price for the same plan.

That's exactly what happened to Ryan and Steph when they needed to cover health care costs.

Their $100,000 IRA withdrawal pushed their income over the 400% line, and they lost their entire ACA subsidy. At 60, each of them was paying $1,350 a month for a basic silver plan, $32,400 a year in premiums alone, all of it coming out of accounts taxed at 22%.

For early retirees covering their own health insurance for a decade or more before Medicare kicks in, managing withdrawals to stay below that income threshold is one of the highest-value decisions in the entire plan. A health savings account (HSA), funded during your working years, can cover some of those costs penalty-free and with favorable tax treatment, but only if it's in place before your retirement date.

3. What Withdrawal Math on a 40-Year Investment Strategy Looks Like

The third problem is pure arithmetic.

Traditional retirement planning uses what's known as the 4% rule as a baseline: if you withdraw 4% of your portfolio in year one and adjust for inflation each year after that, your savings should last about 30 years.

But a 30-year retirement assumes you're leaving work at full retirement age in your mid-60s. Retire in your 50s, and you're looking at 35 to 40 years. Stretching the timeline to 40 years drops the sustainable withdrawal rate to about 3.2%.

Ryan and Steph were pulling at 5.3%, nearly two full percentage points above what their timeline could support. That gap does more than drain a portfolio faster.

When you're withdrawing to cover living expenses and the market drops in your early retirement years, you're liquidating holdings at lower prices because you have no other income source to fall back on. Those shares are gone, and they never get the chance to recover when the market does.

The earlier you retire, the more years that math has to compound against you.

How Coordination Turns a Number Into A Plan

Ryan and Steph didn't have a spending problem. They had a withdrawal problem.

The amount they needed to live on was reasonable. The issue was that pulling it all from pre-tax investment accounts in one lump created a cascade of tax and healthcare costs that made every dollar 42% more expensive than it needed to be.

Coordinated planning is the core of what we build at Seaside Wealth Management, and it works by managing taxes, healthcare costs, and withdrawals as one connected system.

Here's what that looks like in practice:

1. Withdraw From the Right Accounts First

We draw from taxable brokerage accounts first, because those withdrawals are taxed as capital gains rather than ordinary income and don't inflate your MAGI.

2. Do Your Roth Conversions While Your Income Is Low

While your retirement income is low enough to make it worthwhile, we convert traditional IRA dollars to a Roth IRA so that money grows tax-free from then on.

3. Time Every Withdrawal to Stay Below the Thresholds

And we time every withdrawal to stay under the specific thresholds that trigger a higher tax bracket, a Medicare surcharge, or a lost ACA subsidy.

We've seen what Ryan and Steph's retirement looked like without coordination: a 22% effective tax rate, healthcare eating 20% of every withdrawal, and a portfolio eroding faster than either of them realized.

That was before they came to Seaside Wealth Management. After we rebuilt the withdrawal structure, those numbers changed. Their effective tax rate dropped to 9%. Their healthcare costs fell to 12% of spending.

They didn't start spending less money. They enjoyed the same lifestyle they always had. They just stopped losing 42 cents on every dollar to costs that were entirely avoidable.

Early Retirement Planning Is a System, Not a Number

$1.5 million is enough for a successful early retirement. Ryan and Steph prove that.

But an early retirement isn't just about a savings goal. Without the right withdrawal structure, any portfolio can erode faster than anyone expects.

The difference between Ryan and Steph's first five years and everything that came after wasn't more savings or less spending. It was coordination.

That's what we build at Seaside Wealth Management. A system that manages taxes, healthcare costs, and withdrawals together so the retirement you've earned actually lasts the way you planned it.

If you're weighing an early retirement goal, start with our complimentary "Will My Money Last?" Retirement Analysis. We'll show you what your savings can actually support and exactly what needs to be in place before you make your first withdrawal.

Read More

5 Things Conventional Retirement Wealth Management Gets Wrong

5 Retirement Investment Strategies for Modern Longevity

How the Right Retirement Planning Services Determine Whether Your Savings Last

Why $1 of Extra Income Can Cost You $5,000 In Retirement Tax Planning

How Outdated Estate Planning Can Cost The Family It Was Meant To Protect