How the Right Retirement Planning Services Determine Whether Your Savings Last

Every retiree has a vision for how they want to live the rest of their life.

The worry that many of you have is that your savings won't be enough to facilitate it. That puts a tremendous amount of attention on the amount of money and assets you've accumulated heading into retirement.

But the savings you've spent decades building are only half the equation.

For most of your working life, the goal was straightforward: save more, invest consistently, and let time do the rest. That discipline is what got you here, but retirement asks something different of you entirely.

The portfolio that spent decades growing now needs to support 30 years of spending, in a tax environment that penalizes the unprepared, and against inflation that never stops. The focus has to shift from accumulating wealth to sustaining it. Those are two fundamentally different challenges, and they require two fundamentally different plans.

This article walks through what that plan looks like, what it protects you from, and what becomes possible when it's built around your specific financial goals.

What Should Near-Retirees Ask Their Financial Advisor?

Somewhere in their late 50s, many people start doing a similar calculation. They add up their 401(k), their brokerage account, their IRA, maybe their pension, and land on a number.

That number becomes a threshold, a figure that signals they've made it, that the hard part is behind them.

But a number is not a plan.

A portfolio that looks sufficient at retirement age still needs to hold up against inflation, market volatility, rising healthcare costs, and shifting tax law for decades to come.

The question most near-retirees ask their financial advisor — "Do I have enough?" — is a savings question. The real question you should be asking is structural: Is your retirement savings plan structured for how a 30-year retirement actually works?

That's where the real risk lives, and it's the question that the right retirement planning services are designed to answer.

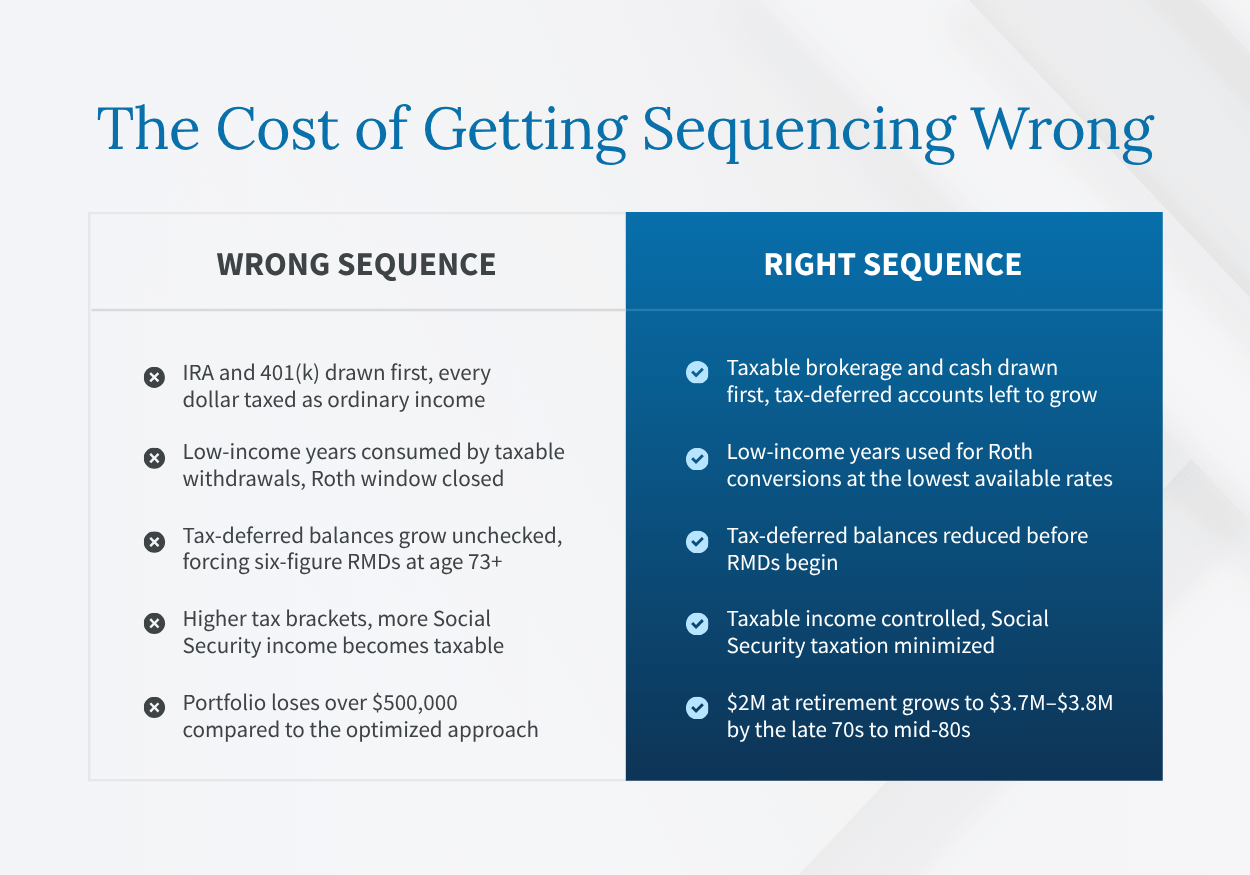

What Happens When Retirement Accounts Are Withdrawn in the Wrong Order

Consider a couple who retires with $2 million spread across a 401(k), a Roth IRA, and a taxable brokerage account.

The funds in their retirement savings accounts are significant. And yet, without a coordinated withdrawal strategy, they can quietly erode that portfolio in ways that never show up in a basic projection.

The most common mistake happens at the very first withdrawal.

When retirees pull income from their tax-deferred retirement accounts first, they trigger ordinary income tax on every dollar they take out. That feels manageable in year one. By year five, something more serious happens.

By then, they’ve used up the low-income years that should have been reserved for Roth conversions, and done nothing to reduce the tax-deferred balance that will eventually become subject to Required Minimum Distributions (RMDs).

The tax implications of this sequencing mistake compound quietly and, once set in motion, can’t be undone.

Starting at age 73, the IRS requires withdrawals from tax-deferred accounts on a fixed schedule, regardless of whether the income is needed. For a retiree with a large tax-deferred balance, that can mean six figures in forced taxable income every year.

This income pushes you into higher brackets, causes more of your Social Security benefits to become taxable, and eliminates the flexibility to do anything about it because the window for Roth conversions at favorable rates has closed.

The consequences of this on your financial future aren't abstract.

What the Wrong Order Actually Costs

Even a couple with a $2 million portfolio that takes distributions from the wrong accounts at the wrong time — no coordinated retirement strategy, no attention to tax brackets — can lose over $500,000 in portfolio value compared to the optimized approach. Their probability of not running out of money drops from 98% to 89%.

For most people at that savings level, running out of money entirely isn't the real risk. The real risk is quieter and harder to see: a retirement that technically survives but never fully delivers.

The $500,000 lost is seen in the travel that gets deferred, the support to family that gets scaled back, the margin that gets spent managing anxiety instead of living. The 9-percentage-point drop in plan confidence might not show up as a crisis. But it does end up as a persistent undercurrent of financial worry that colors every spending decision for the rest of your life.

That doesn't happen because of bad markets or bad luck. It happens because the plan had no structure.

The Investment Strategies Behind a Financial Plan Built to Last 30 Years

A structured retirement plan treats asset allocation, risk management, and tax planning as a single system, because in retirement, none of them work in isolation.

The way a portfolio is allocated determines how long it can sustain withdrawals. The order those withdrawals are taken determines the tax exposure. And the tax exposure determines how much of the portfolio actually reaches the retiree.

Getting that sequence right begins with taxable brokerage accounts and cash reserves, drawn first while tax-deferred accounts continue to grow.

Those early low-income years become the window for Roth conversions, locking in favorable rates before forced distributions take over and close it permanently.

For a couple who executes that sequence with discipline, the results compound in ways a basic projection never captures.

Drawing from the brokerage account first keeps tax-deferred balances growing untouched. Strategic Roth conversions through the gap years reduce the balances that would otherwise generate forced, heavily taxed RMD income later. And a diversified portfolio — structured so that three to five years of living expenses are never at risk from market volatility — stays invested and growing across asset classes that don't move in lockstep.

Those three decisions, made consistently over time, are what take a $2 million starting point to $3.7 million by their late 70s. It’s not dependent on a favorable market or a lucky decade. It’s the result of structure.

How Seaside Wealth Management's Financial Planning Services Deliver This Structure

The Coordinated Retirement Framework is the specific system Seaside Wealth Management's comprehensive retirement planning services build around each client's financial situation.

It's not a portfolio with a withdrawal rate attached. It's a year-by-year income map that coordinates Social Security benefits, portfolio withdrawals, pensions, and cash-flow buffers so that every year of retirement has a clearly defined plan behind it.

A Withdrawal Sequence Built Around Tax Treatment

The sequence is constructed around account type and tax consequence.

Taxable brokerage assets come first, preserving tax-deferred accounts for later. The gap years between retirement and RMD onset become the Roth conversion window — used deliberately to shift balances at low rates before forced distributions make that impossible.

By the time RMDs arrive, the tax-deferred balance has been reduced, the Roth accounts have grown without interruption, and the client controls their taxable income rather than having it dictated by an IRS schedule.

A Multi-Year Tax Strategy That Maps the Full Arc

Our Multi-Year Tax Strategy maps Social Security taxation, provisional income thresholds, Roth conversion windows, and RMD timing across the full arc of retirement.

We know the decisions made in year three directly affect tax exposure in year 15. Treating each year as an isolated tax event misses the compounding consequences (and the compounding opportunities) entirely.

An Investment Structure Built Around Your Numbers

There’s no cookie-cutter allocation. Your investment structure reflects your specific risk tolerance and timeline, with three to five years of living expenses held in stable assets. The rest is positioned across strategies that don’t depend on any single market performing well at any given moment.

The right structure is engineered backward from what you actually need — your spending, your timeline, your tolerance for volatility — using financial science to back into the answer rather than applying a generic model to every situation.

What Happens to Your Financial Goals When the Right Withdrawal Sequence Is in Place

The couple with $2 million in savings that we’ve used as an example throughout this article doesn’t just preserve their retirement savings with a coordinated withdrawal strategy. They grow their retirement income.

The right structure changes something beyond the numbers, too.

With financial stability, a retiree knows exactly where income is coming from each year, which accounts are being drawn and why. When you know your plan has held up against a thousand different market environments, the experience of retirement changes entirely.

It stops being a prolonged exercise in financial anxiety and becomes what it was always supposed to be: the freedom to spend the wealth that took decades to build.

The Right Retirement Advisor Does More Than Managing a Portfolio

Retirement planning services can sometimes be delivered as nothing more than investment management with a different label. The portfolio is managed, returns are reported, and the client is left to figure out the rest.

That’s not good enough for a worry-free retirement with a secure financial future. It’s not what a retirement advisor should be doing.

At Seaside Wealth Management, we deliver coordinated retirement financial planning services that bring income, taxes, investments, and spending together under one integrated system. We help clients make informed decisions from the years leading up to retirement through the decades that follow, building every recommendation around your specific savings, timeline, and retirement goals.

The questions that keep most retirees up at night deserve a real answer. Will your money actually last 30 or more years? Can you grow your wealth throughout retirement instead of watching it drain? Will there be anything left to pass down to your kids?

Our complimentary retirement analysis is a three-part financial review built to answer exactly those questions with a plan built around your numbers, not a generic model.

Schedule your complimentary retirement analysis today.

Read More

5 Things Conventional Retirement Wealth Management Gets Wrong

The Early Retirement Planning Guide To Cut $32K/Year In Avoidable Premiums

5 Retirement Investment Strategies for Modern Longevity

Why $1 of Extra Income Can Cost You $5,000 In Retirement Tax Planning

How Outdated Estate Planning Can Cost The Family It Was Meant To Protect