5 Things Conventional Retirement Wealth Management Gets Wrong

The retirement wealth management industry has a problem.

"Wealth management" is a term that implies something comprehensive. As a result, retirees hire professional advisors assuming they’ll get a system that brings income, taxes, investments, and financial goals together with someone accountable for how all the pieces interact.

What most retirees actually get is money management or investment management with a broader label attached.

That distinction might seem simply semantic at first, but over a 30-year retirement it can cost you hundreds of thousands of dollars.

Portfolio Management Is One Part Of A Bigger Picture

The firms and financial advisors that make up the retirement wealth management industry are, for the most part, structured around one thing: managing a portfolio. They monitor allocations, report returns, and rebalance when the market moves.

What they rarely do — what the industry's design doesn't require them to do — is coordinate the tax decisions, income sequencing, Social Security strategy, and legacy planning that determine how much of that portfolio a retiree actually gets to spend.

The five problems below aren't failures of individual advisors. They're the predictable output of an industry built around the wrong objective.

Instead of building a comprehensive plan designed to sustain your retirement for 30 years, conventional wealth management is focused on one thing — your portfolio — and leaving everything else for you to sort out.

1. Leaving the Wealth Management Industry's Coordination Gap Unaddressed

When your investment advisor, CPA, and estate attorney each work in isolation, the decisions that fall between their lanes don't get made. Coordinated investment advice gets missed.

The Failure

Each professional optimizes for their lane. None of them are accountable for what happens at the intersections.

What This Looks Like for You

A retiree pulls $90,000 from a traditional IRA to fund a kitchen renovation. On the surface, it’s a reasonable decision, but what follows is anything but.

That withdrawal pushes modified adjusted gross income above the IRMAA threshold, triggering Medicare Part B and Part D surcharges for two years. The same income spike makes more of their Social Security benefit taxable under provisional income rules. And because those dollars arrived in a year that could have been used for low-rate Roth conversions, that window closes without anyone noticing it went.

The investment advisor didn't know about the renovation. The CPA saw the numbers after the fact. Other advisors were completely out of the loop. And nobody ran a projection before the withdrawal cleared.

What It Costs

The damage isn’t immediately visible on any account statement. It accumulates over years, across hundreds of small, reasonable-looking decisions.

Over a 20-year retirement, the difference between a retiree who proactively manages provisional income thresholds and one who doesn't can easily exceed six figures in avoidable taxation.

2. Misreading What Retirement Planning Requires at 30 Years

The instinct to de-risk at retirement is understandable. Applied too aggressively, though, it quietly dismantles the growth engine that a three-decade retirement depends on.

The Failure

Too often, wealth advisors let retirees treat the retirement date as a finish line. For a retirement that may last 30 years, it's the starting line for a different race.

What This Looks Like for You

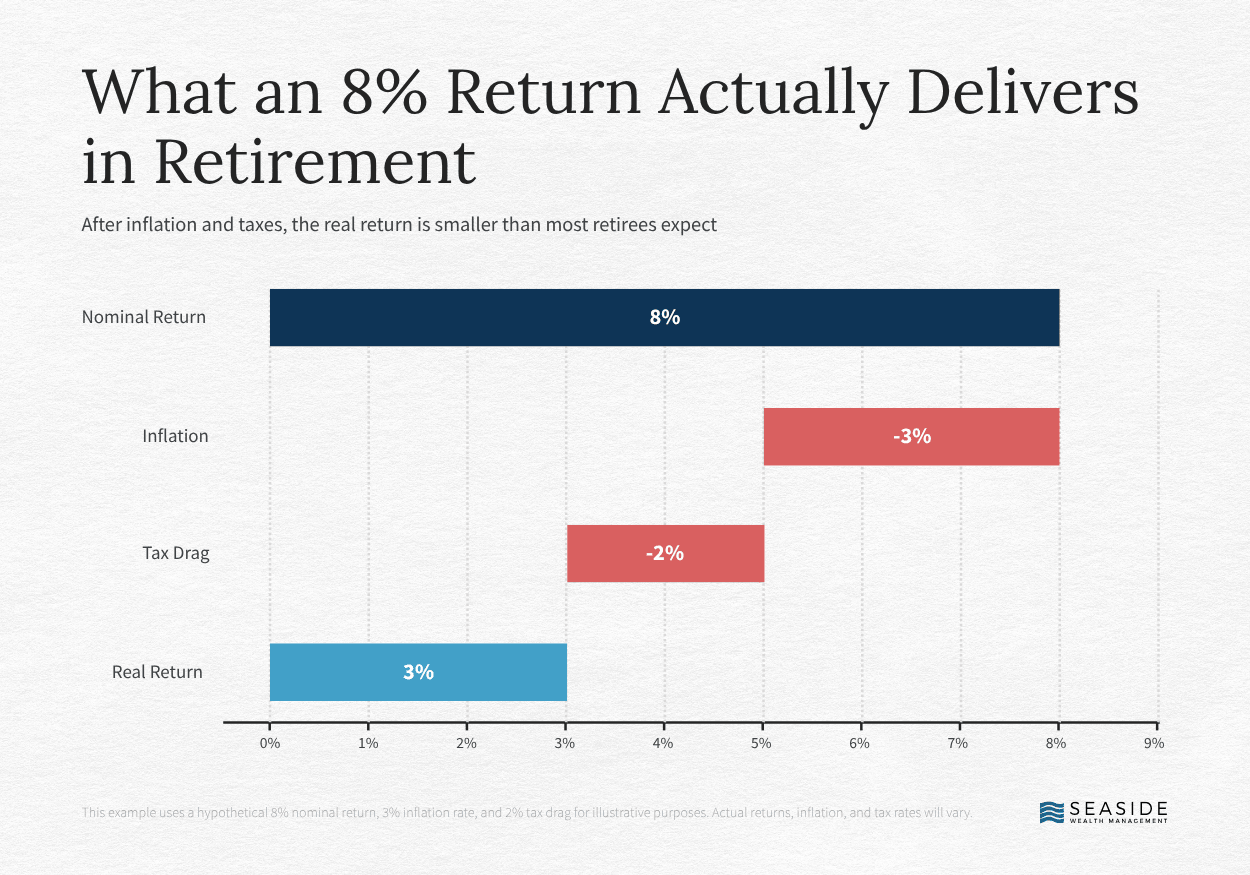

An 8% nominal return sounds healthy until inflation and taxes take their share. Subtract a 3% inflation rate and 2% tax drag and that return drops to roughly 3%. That’s barely ahead of the long-term inflation average.

A portfolio weighted too heavily toward bonds can't sustain that math across two or three decades of rising costs. The retiree who took a conservative allocation at 65 and felt protected at 67 begins to feel the gap at 77.

What It Costs

Getting too conservative too soon feels like risk management. But for a retirement that could last 30+ years, it’s the risk itself. It’s just a slower-moving kind of risk that compounds across every year the portfolio fails to stay ahead of inflation.

3. Treating Social Security as a Date, Not a Financial Planning Decision

Of all the decisions retirement wealth advisors handle, Social Security timing is among the most consequential and among the most frequently undersold.

The Failure

Most advisors treat Social Security as a one-time administrative decision. The reality is it's a multi-year income and tax coordination problem with permanent consequences.

What This Looks Like for You

Claiming at 62 locks in a permanently reduced benefit. Delay to 70 and that benefit grows meaningfully every year in between. That gap, compounded across a long retirement, can represent six figures in foregone lifetime income.

That’s not the only issue at play here. The claiming decision feeds into provisional income calculations, interacts with Roth conversion windows, and affects bracket management across the gap years before RMDs begin.

A wealth manager who handles the Social Security decision without running those projections isn't really doing retirement planning. They’re merely filling in a form.

What It Costs

A suboptimal claiming decision isn't a one-time loss. It's a permanent annual reduction compounding quietly across every remaining year of retirement, with tax consequences layered on top.

4. Letting RMDs Arrive Instead of Managing Them

By the time most financial planners raise the subject of required minimum distributions (RMDs), the decisions that determine their size have already been made.

The Failure

RMDs get treated as an event that happens at 73. They're actually the outcome of every withdrawal, conversion, and income decision made in the years before.

What This Looks Like for You

Required minimum distributions are calculated as a percentage of tax-deferred account balances. The larger the balance, the larger the forced distribution.

A retiree who spent the gap years drawing from the wrong accounts and skipping Roth conversions arrives at 73 with six-figure annual distributions whether the income is needed or not.

Those distributions push taxable income into higher brackets, trigger IRMAA surcharges on Medicare premiums, and make more Social Security income taxable. All simultaneously, with no way to undo any of it.

What It Costs

The gap years between retirement and age 73 are a planning window that closes permanently. A Roth conversion strategy executed during that window reduces RMD exposure, lowers lifetime Medicare costs, and builds a tax-free asset that benefits the retiree and their heirs.

Every year that window goes unused is an irreversible forfeiture.

5. Underestimating What Investment Management Really Costs

Most retirees know their expense ratio as the annual percentage a fund charges to cover its management costs. What they don't know is that it's only part of what they're paying.

The Failure

What doesn't get disclosed is the turnover ratios, tax drag from mutual fund distributions, and redundant holdings. All of these compound silently on top of disclosed fees without every showing up as a line item.

What This Looks Like for You

When a mutual fund manager buys and sells positions inside the fund, those trades generate taxable gains that get passed directly to the investor even if the investor never touched their account.

In 2022, a year when both stocks and bonds declined sharply, investors holding actively managed mutual funds in taxable accounts still received capital gains distributions and owed taxes on gains they never saw. The fund lost money. The tax bill arrived anyway.

The redundancy problem compounds this further. A portfolio built from multiple mutual funds often owns the same securities dozens of times across different funds.

The diversification is largely an illusion. The fees are not.

What It Costs

A disclosed expense ratio of 0.30% on a portfolio with an 87% turnover ratio produces a total cost closer to 1.17%. Compounded across a 20-year retirement, the gap between that portfolio and one built around low-cost, tax-efficient vehicles adds up to hundreds of thousands of dollars in returns that never reach the retiree.

How Smarter Financial Planning Addresses Each of These Problems

A coordinated retirement wealth management plan doesn't just reduce these costs, it eliminates the structural conditions that create them.

Here's how Seaside Wealth Management approaches each one:

The Coordinated Retirement Framework

Every plan starts with a year-by-year income map that integrates Social Security timing, withdrawal sequencing, tax strategy, and investment structure into one connected system.

One team, one plan, full accountability for how every component interacts. That means the decisions that fall between disciplines in traditional wealth management get made, not missed.

Retirement Planning Across Your Full Financial Picture

When the investment decision, the tax decision, and the income decision are made by the same team against the same plan, coordination gaps close before they open.

The renovation gets projected. The Roth window gets used. The RMD balance gets managed down deliberately, years before distributions begin.

A Multi-Year Tax Strategy, Not an Annual Filing Exercise

Social Security optimization, provisional income management, Roth conversion windows, and RMD timing are treated as connected variables in a single multi-year plan instead of separate annual decisions.

Choices made at 64 get evaluated against their effect on tax brackets at 74 and legacy outcomes at 84.

Wealth Management Services Built Around Real After-Tax Returns

Portfolios are built around low-cost, tax-efficient vehicles, including ETFs and, where appropriate, direct indexing strategies in taxable accounts.

Every investment structure is engineered backward from the client's actual spending needs, time horizon, and risk tolerance. Actively managed funds, where they appear, are evaluated against their total cost including turnover, not just the disclosed expense ratio.

What Coordinated Retirement Wealth Management Can Deliver

The lack of coordination is why most retirement plans underdeliver.

It happens quietly across years of decisions that each looked reasonable, made by advisors who each did their job. No one person is to blame. The problem is a system that was never designed to connect wealth to lasting financial security.

Seaside Wealth Management’s approach is built around a clear, integrated framework: a spending plan designed for modern longevity, a year-by-year income map, a multi-year tax strategy, a coordinated withdrawal sequence, and guardrails for family support.

Every component is connected. Every decision is evaluated against its effect on the whole.

Retirement today can last 30 years or more. That reality requires discipline over decades and a plan built to endure for decades, not just perform year to year.

Stop trying to chase hot markets and quick returns with your savings. Reach out to us today to start planning for how you want to live the rest of your life.

Read More

The Early Retirement Planning Guide To Cut $32K/Year In Avoidable Premiums

5 Retirement Investment Strategies for Modern Longevity

How the Right Retirement Planning Services Determine Whether Your Savings Last

Why $1 of Extra Income Can Cost You $5,000 In Retirement Tax Planning

How Outdated Estate Planning Can Cost The Family It Was Meant To Protect