5 Retirement Investment Strategies for Modern Longevity

Your parents didn't have Google Maps.

They had paper maps, gas station atlases, and the occasional hand-drawn directions from someone who'd been there before. Those tools worked for the roads that existed, but would you use them today?

Retirement investing is similar.

Many people carry a philosophy into retirement based on how a previous generation navigated a completely different situation. Your parents retired, collected a pension, leaned on Social Security retirement benefits, and planned for the next 15 years. With that scenario, a conservative retirement savings plan makes sense. Investments were a backup for a retirement that might last 15 years.

But that same generation never had to navigate a Roth conversion ladder, optimize around Medicare IRMAA thresholds, or build an investment portfolio designed to run for 30 years or more.

Think about what a gallon of gas cost in 1996. Many of today's retirees will have a retirement that stretches just as far into the future as 1996 sits in the past.

That's the distance your portfolio needs to cover, and this guide maps the route.

Why Your Parents' Retirement Investment Strategy No Longer Applies

For most of the 20th century, retirement savings plans followed a clear arc: Accumulate aggressively during your working years through your pre-retirement income and an employer-sponsored retirement plan, then shift into bonds at retirement.

Pensions covered the baseline, Social Security benefits filled the gap, and investments were the reserve that would hopefully result in something left over for loved ones.

But a healthy 65-year-old today has a meaningful probability of a 30-year retirement.

Pensions have largely vanished. Inflation has reminded everyone that prices from 25 years ago bear no resemblance to today's.

Every one of those shifts pushes in the same direction, meaning that the strategies that solved a 15-year retirement now actively work against a 30-year one.

The stakes are different now. So is the math.

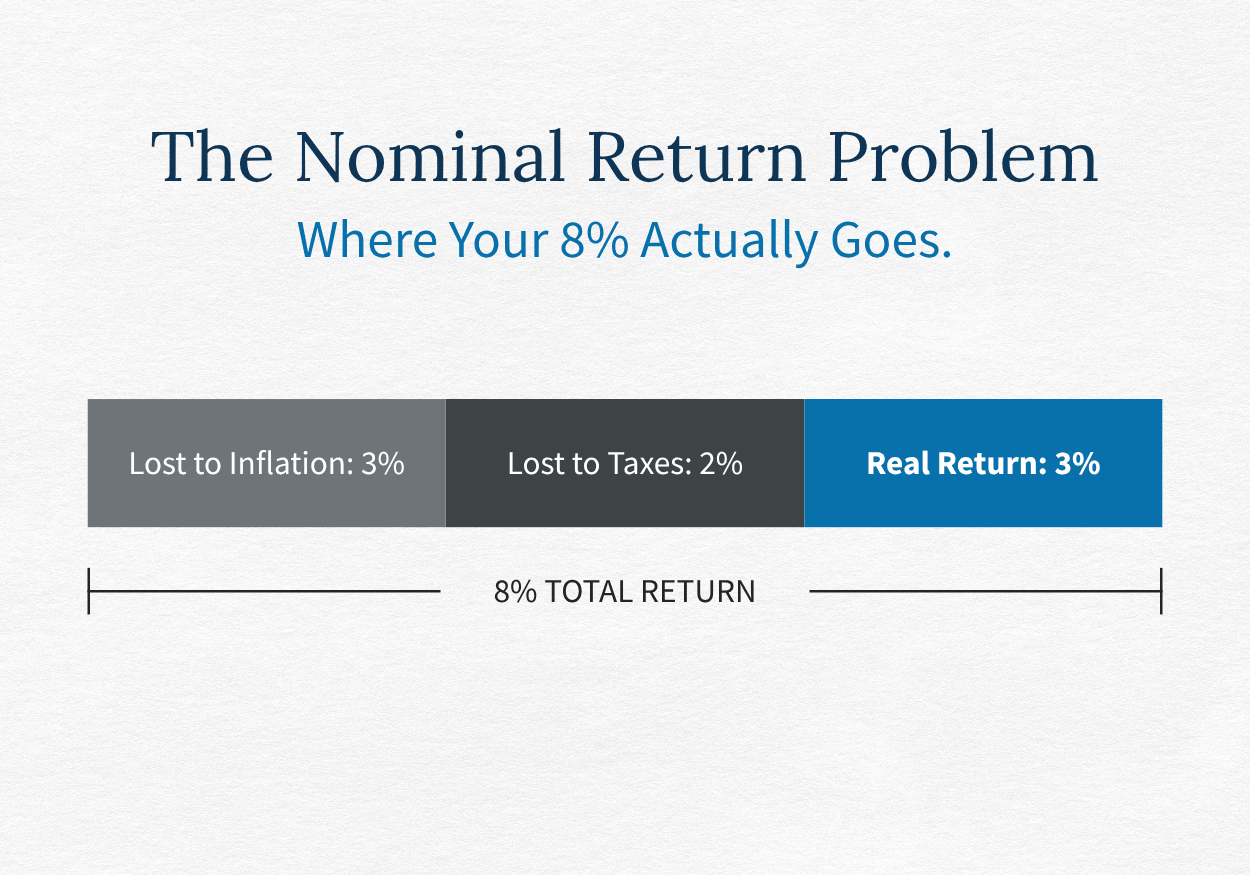

1. Don't Settle For A Nominal Return To Cover Future Expenses

Traditional retirement savings accounts were evaluated by nominal return or the headline percentage. But what matters across a 30-year retirement is the real return: what remains after inflation and taxes.

An investment portfolio generating 8% annually sounds strong. But subtract 3% for inflation and the real gain drops to 5%. Subtract taxes and the after-tax return lands closer to 3%.

A retiree who shifts entirely into low-yield fixed income investments may find their portfolio losing ground without ever showing a loss on paper.

The risk most retirees face isn't a bad year in the market. It's the slow erosion of purchasing power across three decades of future expenses through a conservative portfolio not built for the distance modern retirement demands.

2. Keep Growing Your Retirement Portfolio With The Right Investment Planning

Instead of thinking about it in terms of conservative vs. aggressive, think about it this way...

A retirement portfolio has one job: It needs to pay for the desired retirement lifestyle you've worked toward while keeping up with expenses and rising prices.

That requires growth. You need steady gains that outpace inflation year after year.

Stocks have delivered that better than any other asset class over long stretches of time.

The old rule of thumb was 60% stocks and 40% bonds. With retirements now stretching 25 or 30 years, many advisors have shifted toward 70% stocks and 30% bonds to give the portfolio more room to grow.

But templated approaches to growth won't provide the right answer either. Asset allocation is personal, and it depends on a few things:

- Your risk tolerance and how comfortable you are with market fluctuations

- Your retirement income needs and how much cash flow you'll pull each year

- How much guaranteed income stream you already have from Social Security retirement benefits

Again, this requires a mindset shift.

Traditionally, retirement was seen as a means of protecting what you have. But modern longevity has made retirement investing a matter of making sure what you have keeps working for the next 30 years.

That requires a structure that lets you stay invested even when the market drops.

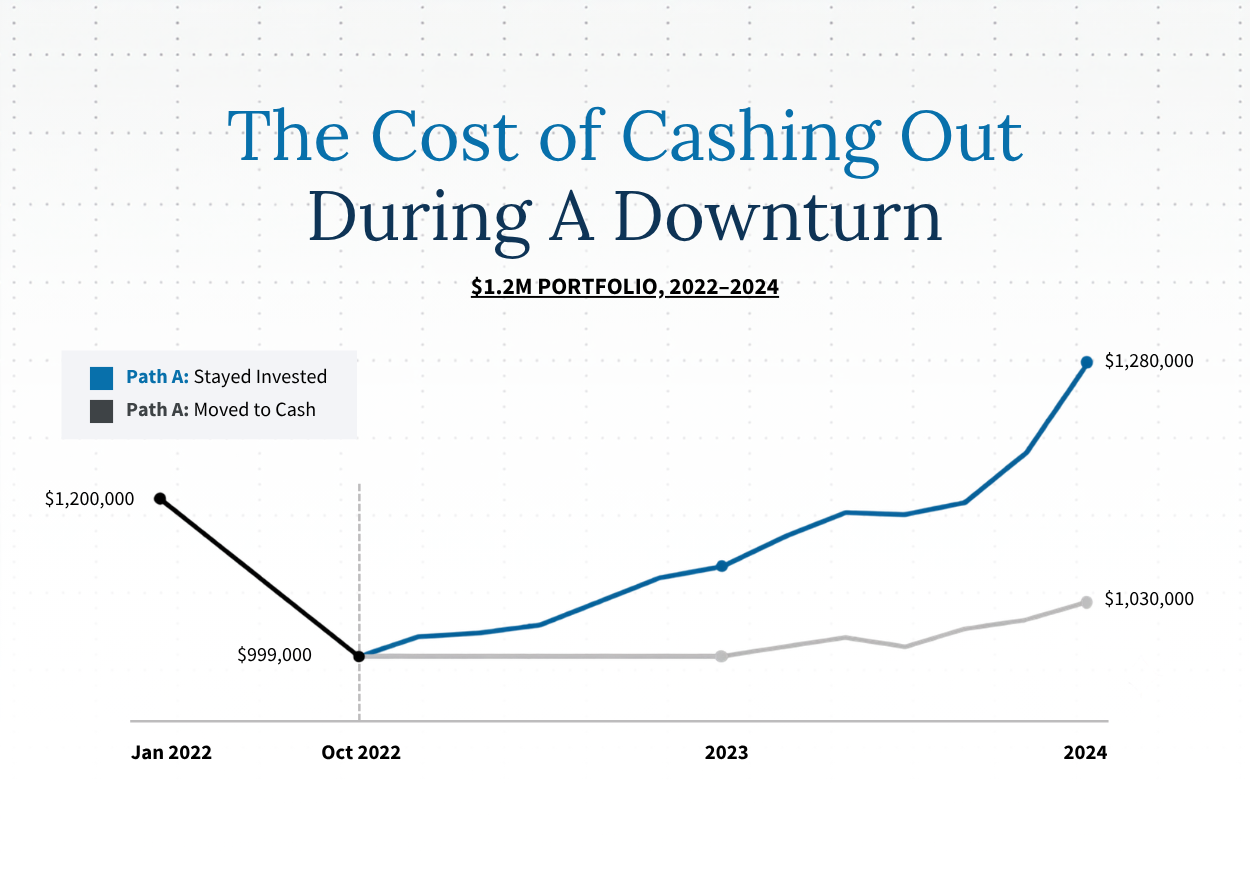

3. Stay Invested Without Selling at the Wrong Time

Stocks grow your money, but you still need cash to live on now.

Most retirees treat their savings as one big pile, so when the market declines, they end up selling stocks at the worst possible time to cover living expenses.

Time segmentation fixes that by splitting your money into three pools based on when you'll spend it. The money you need soon stays safe. The money you won't touch for years stays invested. The middle pool bridges the gap.

Underneath all of this sits a cash reserve of one to two years of living expenses, held in a savings or money market account currently earning north of 4%.

That reserve is what makes the whole structure work. When market conditions turn, you don't have to sell anything to cover near-term retirement expenses.

Years 1 Through 5

The money you'll spend in the near term stays in safe accounts like savings or money market funds. It isn't in the stock market, so it can't drop when you need it. Reliability matters more than growth here.

Years 6 Through 15

This middle pool is a mix of dividend paying stocks, bond funds, and moderate-growth investments. It has enough time to recover from market fluctuations while still generating returns and dividend payments along the way to cover future expenses.

Years 15 and Beyond

Money you won't touch for over a decade can be invested more aggressively across different asset classes. Over a stretch that long, the bigger threat isn't a market drop — it's inflation risk quietly eroding what your money can buy. A Roth IRA is a natural home for this pool, since it grows tax-free and never forces you to take money out.

That ability to ride out bad years without touching the growth side of the portfolio is one of the most valuable things any retirement income strategy can give you.

But structure only works if you use it.

A written plan, made in calm moments with your financial advisor, tells you in advance what you'll do when markets drop.

Follow through with that direction, even when pressure arrives.

4. Build A Diversified Investment Portfolio

Structure keeps you invested throughout market downturns. Diversification is supposed to keep that investment protected.

The problem is that most retirees believe they have a diversified portfolio when they don't.

Mutual funds and ETFs are built from baskets of stocks, and the most popular ones tend to reach for the same handful of dominant companies. Apple, Microsoft, Nvidia, Amazon. The names show up again and again, across fund after fund, until a portfolio that looks broad on paper is really just the same dozen companies in different costumes.

At Seaside Wealth Management, we saw this firsthand with a client we'll call Mr. Diversified.

Mr. Diversified came in for a portfolio audit feeling confident about his retirement savings accounts. The audit told a different story: 32 mutual funds, 21 ETFs, and over 93,000 individual stock positions.

Even though there are roughly 53,000 publicly traded stocks worldwide, he was holding the same stocks over and over. Microsoft alone appeared in 10 of his funds simultaneously.

Real diversification means owning pieces of different markets, not just different fund names.

5. Add Three Layers of Tax-Strategy to Your Retirement Planning

Building the right investment portfolio is half the equation. The other half is understanding the tax implications of where your money is held and when you take it out.

Small, consistent tax efficiency can compound just as powerfully as investment growth over 30 years or just as destructively when ignored.

Layer #1: How Your Investments Are Taxed

Different investments carry different tax treatment, and most retirees discover this at tax time rather than in advance. The result is almost always a higher tax burden than necessary.

For instance, capital gains on investments held longer than one year are taxed far more favorably than the ordinary income tax rates that apply to short-term gains.

For 2026, married couples filing jointly pay 0% on long-term gains up to $98,900 in taxable income. Missing the one-year-and-a-day threshold by a single day can mean the difference between 0% and 22% on the same gain.

But that's just one tax insight to be aware of. There are several more related to taxes on qualified dividends from large domestic companies vs. ordinary dividends, bond interest vs. municipal bonds.

And then there are different taxes for different funds. REITs are taxed mostly as ordinary income, while gold ETFs are taxed as collectibles at up to 28%.

Taking this type of information into account in advance, rather than at tax time, is how you build a retirement income strategy that doesn't quietly overpay year after year.

Layer #2: Where You Hold Each Investment Option

Most retirees focus on asset allocation (what they own).

Fewer focus on asset location (where they hold it).

But that's where some of the largest available tax benefits are quietly captured or surrendered.

Tax-inefficient assets belong in tax deferred accounts like a traditional IRA or 401(k), where distributions are taxed later. Tax-efficient assets belong in taxable accounts, where their preferential treatment — qualified dividends, long-term gains — can be fully realized. Meanwhile, Roth IRA contributions are best matched to the highest-growth, longest-horizon positions, since every dollar of investment growth in those tax free accounts stays intact.

Asset location also carries estate planning implications. Taxable accounts passed to heirs receive a step-up in basis with no embedded capital gains liability. Inherited IRAs now carry a 10-year distribution requirement under the SECURE Act, often forcing heirs to withdraw during peak earning years at their highest tax rates.

Which retirement account to draw down and which to preserve is a meaningful part of any coordinated financial plan.

Layer #3: Managing Your Tax Brackets By Looking Ahead

Asset location determines where you hold things. Tax bracket management determines when and how you move money out.

Instead of thinking of tax brackets as a constraint to avoid, consider them a resource to use.

For 2026, the 12% bracket for married couples filing jointly runs up to $100,800. The 22% bracket runs up to $211,400. Those ceilings create defined windows for deliberate action.

The gap between retirement and required minimum distributions at age 73 is often the lowest-income window of a retiree's life. Converting traditional IRA funds to a Roth during those years means paying tax at today's lower tax bracket rather than at higher rates when RMDs force larger distributions later.

For retirees with taxable income below $98,900, long-term gains in taxable accounts are federally tax-free. Taking advantage of this creates an annual window to rebalance or generate income at zero cost.

When positions decline, tax-loss harvesting locks in a deduction that offsets gains dollar-for-dollar and reduces ordinary income by up to $3,000 per year.

These savings strategies require looking at your financial plan each year, but the moves you make should always be aligned to how it will impact the taxes you pay through your entire retirement.

This requires someone to coordinate everyone working on your behalf, from the qualified tax advisor to your financial advisor.

Build Investment Growth Into Your Retirement Plan

A retirement built to last 30 years looks nothing like one built to last 15.

It needs more growth to outpace inflation, deliberate thinking about asset location and tax implications, real diversification across asset classes, and a written plan that decides for you in advance what you'll do when market volatility arrives.

The instinct to play it safe isn't wrong. It's just aimed at the wrong risk.

Instead of a single bad year on the stock market, it's the quiet accumulation of small inefficiencies like tax drag, redundant fees, and an overly conservative investment strategy compounding against you across three decades.

If reading this has you wondering whether your own retirement savings plan is built for the distance ahead, reach out to us today.

Schedule a complimentary "Will My Money Last?" Retirement Analysis with Seaside Wealth Management to talk through your retirement timeline, your income needs, and what a coordinated plan for a secure retirement could look like for you.

Read More

5 Things Conventional Retirement Wealth Management Gets Wrong

The Early Retirement Planning Guide To Cut $32K/Year In Avoidable Premiums

How the Right Retirement Planning Services Determine Whether Your Savings Last

Why $1 of Extra Income Can Cost You $5,000 In Retirement Tax Planning

How Outdated Estate Planning Can Cost The Family It Was Meant To Protect